")

wtstock

If you’re like me, your income from money market funds has increased in recent years. The funds, which invest in short-term, low-risk debt securities, have benefited from Fed interest rate hikes, making them a convenient place to park proceeds from stock sales and dividends.

U.S. money market funds manage over $6 trillion in assets, double the amount in 2018. The most recent seven-day return on the fund offered by my broker was 5.14%, up from nearly zero a few years ago.

Unfortunately, that parking space is about to get even tighter. The Fed’s rate cuts will likely begin in September. Money market rates will follow closely. Investors who want to maintain or even increase their income levels will likely have to move into the riskier world of longer-term corporate bonds.

My long-term investment Wells Fargo 7.5% Preferred Series L (WFC.PR.L) fits the bill. I wrote about it for the first time in one of my first Seeking Alpha articles in January 2016, right after I quit my job at the newspaper. I have been receiving quarterly dividends since then.

The non-cumulative convertible bond has an unusual history and a base value of $1,000 (quantum description). It was issued by Wachovia Corp. at the beginning of the 2008 financial crisis and was acquired by the more solid Wells Fargo at the end of the same year as part of the government-forced sale of Wachovia. As a result, the terms for investors are more favorable than those normally offered by central banks.

It pays a quarterly dividend of $18.75 or $75 annually. It is subject to the 15% preferential tax rate for most taxpayers. At the current price of around $1,208, that gives a yield of about 6.2%.

Unlike most preferred stock, this one can never be called, although it could be converted into common stock in unlikely circumstances. If Wells Fargo (NYSE:WFC) closes above $203.72 for 20 out of 30 consecutive trading days, the company could convert WFC.PR.L into 6.2814 shares of WFC.

However, WFC is only trading at about a quarter of its conversion price, and for practical purposes the market views this preferred stock as perpetual, so if interest rates fall as expected, the price should rise without being constrained by call risk.

Comparative analysis

Let’s compare it to another Wells fixed-rate preferred stock, WFC.PR.Y (Quantum description). The 5.625% coupon issue sells for about $24, which represents a lower yield of 5.86%. Moreover, it could be called immediately if rates fall and Wells could refinance more cheaply, and the company has never been shy about doing so.

The yield gap of up to 60 basis points is shown in this table of Wells preferred shares:

| ticker | coupon | dividend | Last price | Yield | Call date |

| WFC-L | 7.50% | $75 | $1,208 | 0.0621 | Convertible |

| WFC-A | 4.70% | 1,18 € | 20.74 | 0.0569 | 15.12.2025 |

| WFC-C | 4.38% | 1,09 € | 19.45 | 0.056 | 15.03.2026 |

| WFC-D | 4.25% | $1.06 | 18.83 | 0.0563 | 15.9.2026 |

| WFC-Y | 5.63% | 1,41 € | 24.1 | 0.0585 | 15.09.2022 |

| WFC-Z | 4.75% | 1,19 € | 20.66 | 0.0576 | 15.03.2025 |

Source: Author’s research, Charles Schwab

Over the years, I have wondered why the yield gap remains as it is. It seems to be a combination of lower retail interest due to the high price, confusion over difficult to understand conversion terms, and the volatility inherent in a long-dated security.

Another comparison is with Bank of America’s similar $1,000 base rate preferred, the 7.25% BAC.PR.L. This recently yielded slightly less than WFC.PR.L’s 6.01%. It also carries a higher conversion risk, with BAC common securities selling for about 60% of the conversion price, compared to about 25% for the Wells security.

Risk factors

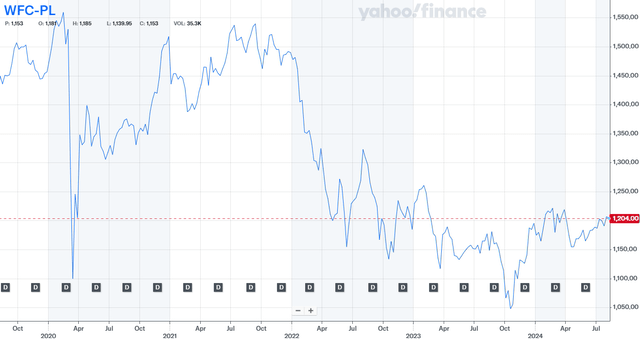

Even with a huge and well-capitalized bank, there is some risk that the dividend could be suspended. This chart shows that the stock has encountered obstacles during market crises, but has always paid dividends and recovered quickly.

WFC’s preferred L-diagram (Google)

A greater risk is that a rise in interest rates could lead to a decline in prices in the next upswing in the economic cycle.

Diploma: WFC.PR.L appears undervalued relative to other money center preferred stocks. I recently bought more, putting it back above a trio of tech winners as the largest position in my portfolio.