posts solid earnings, but there is not all good news")

Kumyang Green Power Co., Ltd.s (KOSDAQ:282720) rose after releasing a solid earnings report. While the headlines were strong, we found some underlying issues when we looked at the factors affecting earnings.

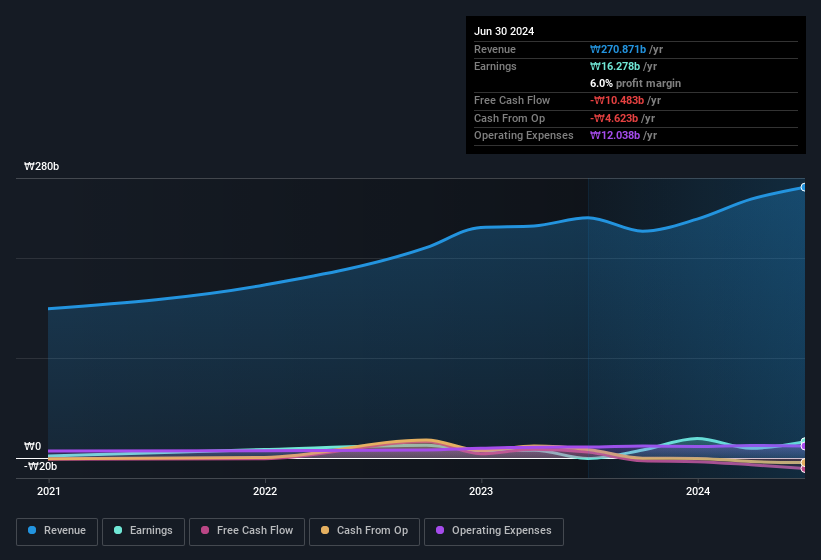

Check out our latest analysis for Kumyang Green Power

Zoom in on Kumyang Green Power’s revenues

An important financial metric that measures how well a company converts its profit into free cash flow (FCF) is the Delimitation ratio. The accrual ratio subtracts FCF from profit for a given period and divides the result by the company’s average funds from operations for that period. You could think of the accrual ratio from cash flow as the “non-FCF profit ratio.”

Therefore, it is actually considered good if a company has a negative accrual ratio, but bad if its accrual ratio is positive. This is not to say that we should be concerned about a positive accrual ratio, but it is worth noting if the accrual ratio is quite high. In particular, there is some academic evidence to suggest that a high accrual ratio is generally a bad sign for short-term earnings.

In the twelve months to June 2024, Kumyang Green Power recorded a provisioning ratio of 0.36. Therefore, we know that its free cash flow was significantly lower than its statutory profit, which raises the question of how useful this profit number really is. Last year, it actually had Negative free cash flow of ₩10 billion, as opposed to the ₩16.3 billion in profit mentioned above. It’s worth noting that a year ago, Kumyang Green Power generated positive FCF of ₩5.9 billion, so at least they have managed that in the past. However, as we’ll discuss below, we can see that the company’s accrual ratio was impacted by its tax situation. This would partially explain why the accrual ratio was so poor. One positive for Kumyang Green Power shareholders is that the accrual ratio was significantly better last year, giving reason to believe that the company could return to stronger cash conversion in the future. Shareholders should expect improved cash flow to profit in the current year, if that is indeed the case.

Note: We always recommend investors to check balance sheet strength. Click here to access our balance sheet analysis of Kumyang Green Power.

An unusual tax situation

In addition to the notable provisioning ratio, we can see that Kumyang Green Power received a tax benefit of ₩4.7 billion. It’s always a little remarkable when a company gets paid by the taxman rather than paying the taxman. Receiving a tax benefit is a good thing in itself, of course. And given last year’s losses, it seems possible that the benefit is evidence that the company now expects to recoup its previous tax losses. However, our data shows that tax benefits can temporarily boost statutory profit in the year they are recorded, but can decline later. In the likely event that the tax benefit is not repeated, we would expect statutory profits to decline, at least absent strong growth.

Our assessment of Kumyang Green Power’s earnings development

This year, Kumyang Green Power has failed to match its profit with cash flow. Unless the tax benefit repeats, next year’s profit would fall if everything else remains unchanged. For the reasons outlined above, we believe a cursory glance at Kumyang Green Power’s statutory profits could make the company look better than it actually is at an underlying level. So if you want to dig deeper into this stock, it’s important to consider all the risks it faces. For example, Kumyang Green Power has 3 warning signs (and 1 that is concerning) that we think you should know about.

In this article, we have looked at a number of factors that can affect the usefulness of earnings numbers, and we have proceeded with caution. However, there are many other ways to form an opinion about a company. Some people consider a high return on equity to be a good sign of a high-quality company. Although you may need to do a little research, you may find free Collection of companies with high return on equity or this list of stocks with significant insider holdings may prove useful.

Valuation is complex, but we are here to simplify it.

Find out if Kumyang Green Power could be undervalued or overvalued with our detailed analysis, Fair value estimates, potential risks, dividends, insider trading and the company’s financial condition.

Access to free analyses

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.