still has a long way to go to become a multibagger")

To find a multi-bagger stock, what underlying trends should we look for in a company? Typically, we want to identify a trend of growth return on the capital employed (ROCE) and in parallel a growing base of the capital employed. Simply put, these types of companies are compound interest machines, meaning that they continually reinvest their profits at ever higher returns. According to the study Energy recovery (NASDAQ:ERII) – we don’t think the current trends fit the mold of a multi-bagger.

Return on Capital Employed (ROCE): What is it?

For those who don’t know what ROCE is, it measures the amount of pre-tax profit a company can generate with the capital employed in its business. To calculate this metric for Energy Recovery, the formula is:

Return on capital = earnings before interest and taxes (EBIT) ÷ (total assets – current liabilities)

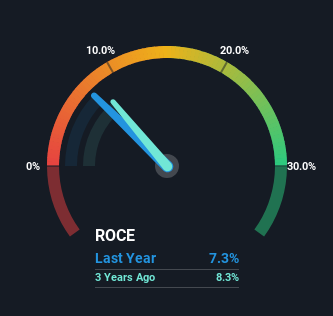

0.073 = $17 million ÷ ($249 million – $20 million) (Based on the last twelve months to June 2024).

So, Energy Recovery has a ROCE of 7.3%. Ultimately, this is a low return and is below the industry average of 14% in mechanical engineering.

Check out our latest energy recovery analysis

Above you can see how the current ROCE for Energy Recovery compares to previous returns on capital, but there is only so much to infer from the past. If you want, you can look at the analyst forecasts that Energy Recovery has for free.

The trend of ROCE

There are better returns on capital than what we see at Energy Recovery. Over the past five years, the return on capital has remained relatively stable at around 7.3%, and the company has invested 44% more capital in its operations. Given that the company has increased the amount of capital employed, the investments being made simply do not seem to offer a high return on capital.

The most important things to take away

In summary, Energy Recovery has simply reinvested capital and delivered the same low returns as before. However, for long-term shareholders, the stock has delivered an incredible 100% return over the past five years, so the market is looking bright for the future. If the underlying trends continue, we would not expect the company to become a multibagger in the future.

We also found 2 warning signals for energy recovery You probably want to know more about it.

For those who like to invest in solid companies, look at this free List of companies with solid balance sheets and high returns on equity.

Valuation is complex, but we are here to simplify it.

Discover whether energy recovery might be undervalued or overvalued with our detailed analysis, with Fair value estimates, potential risks, dividends, insider trading and the company’s financial condition.

Access to free analyses

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.